Can You Set Up a Trust Without an Attorney? Complete DIY Guide (Steps, Costs & Risks)

Introduction

A trust is an important estate planning tool that allows a person to manage and distribute their assets according to their wishes. It creates a legal arrangement where one party holds and manages property or assets for the benefit of another. Many individuals use trusts to avoid probate, protect assets, and ensure their wealth is transferred smoothly to beneficiaries after their death.

A common question people ask during estate planning is: can you set up a trust without an attorney? The short answer is yes. In many cases, individuals can create a basic trust on their own by using online tools, trust templates, or estate planning software. However, while a do-it-yourself (DIY) trust can work for simple estates, it also carries certain risks if the documents are prepared incorrectly or if important legal steps are missed.

Creating a trust without a lawyer can offer several advantages, such as lower costs and faster setup. At the same time, it requires careful attention to legal details, proper documentation, and correct asset transfers. Understanding both the benefits and the potential risks is essential before deciding whether a DIY trust is the right option for your situation.

Featured Snippet Answer

Yes, you can set up a trust without an attorney by creating a trust document, naming a trustee and beneficiaries, signing the document legally, and transferring assets into the trust. However, DIY trusts are generally best for simple estates and may not be suitable for complex financial or legal situations.

What Is a Trust in Estate Planning?

A trust is a legal arrangement used in estate planning to manage and distribute assets for the benefit of another person or group. In simple terms, a trust allows one person to place their property, money, or investments under the control of a trusted individual or organization, which then manages those assets according to specific instructions.

Trusts are commonly used to ensure that assets are handled responsibly and passed on to beneficiaries in an organized and legally recognized way. Unlike a simple will, a trust can provide more control over how and when assets are distributed. For example, a trust can specify that funds should only be given to a beneficiary after they reach a certain age or milestone.

Another key advantage of trusts is that they can help streamline the transfer of assets after death and may reduce legal complications for family members. Because of these benefits, trusts are often used by individuals who want to protect their assets, plan for the future of their loved ones, or manage wealth across generations.

Understanding how a trust works begins with knowing the key roles involved in the trust structure.

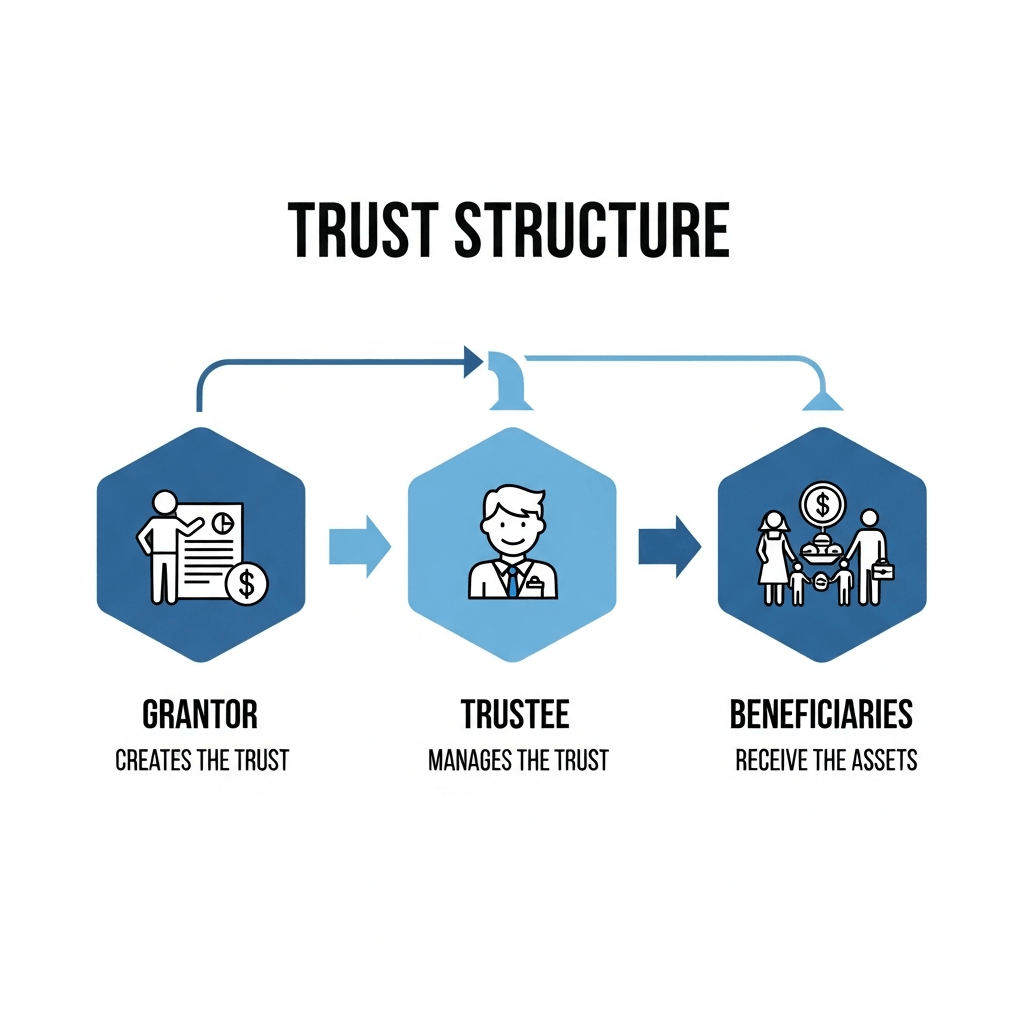

Key Roles in a Trust

Every trust involves three main parties. Each role has a specific responsibility in ensuring the trust operates properly.

Grantor

The grantor (sometimes called the settlor or trustor) is the person who creates the trust. This individual places assets into the trust and sets the rules that determine how those assets will be managed and distributed. The grantor decides who the trustee will be and who the beneficiaries are.

Trustee

The trustee is the person or entity responsible for managing the trust and carrying out the instructions established by the grantor. Trustees have a legal duty to act in the best interests of the beneficiaries. Their responsibilities may include managing investments, protecting trust assets, and distributing funds according to the trust document.

Beneficiaries

Beneficiaries are the individuals or organizations that receive the benefits of the trust. They may receive income, property, or other assets from the trust depending on the terms set by the grantor. Beneficiaries can include family members, children, spouses, charities, or other designated recipients.

Why People Create Trusts

People create trusts for several practical and legal reasons. A well-structured trust can provide financial protection, simplify estate planning, and ensure that assets are distributed according to the grantor’s wishes.

Avoid Probate

One of the most common reasons for creating a trust is to avoid probate. Probate is the legal process through which a court verifies a will and oversees the distribution of assets after someone passes away. Assets placed in a trust can often bypass this process, allowing beneficiaries to receive their inheritance more quickly and privately.

Asset Protection

Trusts can also help protect assets from certain legal risks. Depending on the type of trust used, assets may be shielded from creditors, lawsuits, or financial mismanagement. This makes trusts an important tool for individuals who want to safeguard wealth for their family.

Control Inheritance Distribution

Another advantage of trusts is the ability to control how and when assets are distributed. Instead of giving beneficiaries a large sum of money all at once, the grantor can set conditions or timelines for distributions. For example, funds may be released gradually, used for education expenses, or managed until a beneficiary reaches a certain age.

Because of these benefits, trusts play an important role in modern estate planning strategies. In the next section, we will look at whether it is legally possible to create a trust without hiring an attorney and when doing so may or may not be a good idea.

Can You Legally Set Up a Trust Without an Attorney?

Yes, in many cases you can legally set up a trust without hiring an attorney. Trust laws in most states allow individuals to create their own trust documents as long as the document meets certain legal requirements. These requirements generally include clearly identifying the grantor (the person creating the trust), the trustee who manages the assets, and the beneficiaries who will receive the assets. The trust document must also be properly signed and, in many situations, notarized to ensure it is legally valid.

Today, many people create trusts using DIY trust templates or online legal services. These tools guide users through the process of drafting a trust agreement and organizing their assets. However, while creating a trust without an attorney is possible, it is important to understand that the process still requires careful attention to legal details. Mistakes in wording, incorrect asset transfers, or failure to properly fund the trust can cause legal complications later.

In simple situations, a DIY trust can work well and help individuals save money on legal fees. But in more complex financial or family situations, working with an estate planning attorney may be the safer choice.

When a DIY Trust Is Usually Safe

In certain situations, creating a trust without an attorney can be a practical and cost-effective option. If your financial and family situation is straightforward, a DIY trust may meet your needs.

Simple Assets

A DIY trust works best when your assets are easy to manage and transfer. For example, if you only have a primary home, a savings account, or a few basic investments, transferring those assets into a trust is generally a simple process.

Small Estate

Individuals with smaller estates often choose to create a trust without legal assistance. When the total value of assets is relatively modest and there are no complicated ownership structures, the risk of legal issues is lower.

Single Beneficiary

If the trust has only one beneficiary—such as a spouse or an adult child—the structure of the trust is usually straightforward. With fewer parties involved, there is less chance of disputes or confusion about how the assets should be distributed.

In these types of situations, many people successfully create a revocable living trust on their own using reliable templates or online legal platforms.

When You Should Hire an Attorney

Although DIY trusts can work for simple estates, there are situations where professional legal guidance is strongly recommended. Complex financial or family circumstances often require a carefully customized trust document.

Large Estates

If your estate includes significant assets, multiple properties, or a large investment portfolio, creating a trust without legal advice can be risky. Estate planning attorneys can help structure the trust to reduce tax liability and protect assets more effectively.

Business Ownership

Owning a business adds another layer of complexity to estate planning. Business interests may require special legal language in the trust document to ensure proper ownership transfer and operational continuity.

Complex Tax Situations

Trusts can have important tax implications. If your estate involves complicated tax planning—such as minimizing estate taxes or managing multiple income sources—an attorney can help structure the trust in a way that avoids costly mistakes.

In these cases, hiring an experienced estate planning attorney can help ensure that the trust is legally sound and tailored to your specific financial goals.

Types of Trusts You Can Create Without a Lawyer

When people ask “can you set up a trust without an attorney?”, the answer often depends on the type of trust you want to create. Some trusts are relatively simple and can be created using DIY legal documents or online tools, while others may involve complex legal rules and tax considerations.

Understanding the different types of trusts can help you decide whether creating one on your own is practical or if professional legal guidance is necessary. Below are some of the most common trusts individuals consider when setting up an estate plan.

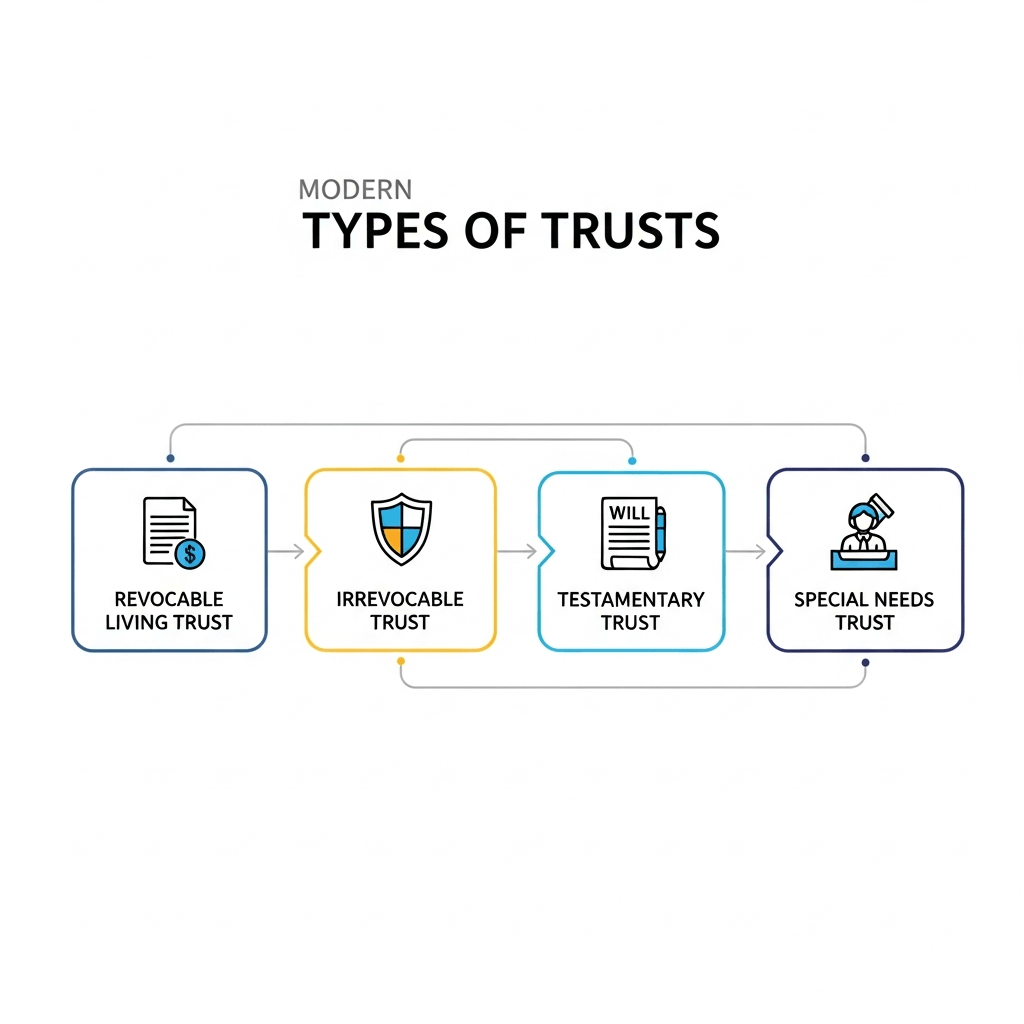

Revocable Living Trust

A revocable living trust is one of the most common types of trusts used in estate planning. It allows the person creating the trust (known as the grantor) to maintain control over their assets during their lifetime.

With a revocable living trust, you can change or revoke the trust at any time as long as you are mentally competent. Many individuals choose this type of trust because it helps avoid probate and allows assets to transfer to beneficiaries more smoothly after death.

Because the structure is relatively straightforward, many people choose to create a revocable living trust without hiring an attorney, especially when their estate is simple and includes common assets such as a home, savings accounts, or investments.

Irrevocable Trust

An irrevocable trust is different from a revocable trust because it generally cannot be changed or canceled once it has been created. When assets are transferred into this type of trust, the grantor typically gives up ownership and control over them.

People often use irrevocable trusts for purposes such as asset protection, estate tax reduction, or protecting wealth for future generations. Since these trusts involve stricter legal rules and financial implications, they can be more complicated to establish without professional help.

While it is technically possible to create an irrevocable trust without an attorney, many individuals prefer to seek legal advice to ensure the trust is structured correctly.

Testamentary Trust

A testamentary trust is created through a will and only becomes active after the person who created it passes away. This type of trust is commonly used when someone wants to control how assets are distributed to beneficiaries over time.

For example, a parent may establish a testamentary trust to manage assets for minor children until they reach a certain age. Because this trust is written into a will, it typically goes through the probate process before being activated.

Some people prepare testamentary trusts themselves using estate planning templates, but the wording in a will must be precise to avoid legal disputes later.

Special Needs Trust

A special needs trust is designed to provide financial support to a person with disabilities without affecting their eligibility for government benefits such as Medicaid or Supplemental Security Income (SSI).

These trusts allow funds to be used for expenses that improve the beneficiary’s quality of life, such as medical care, education, transportation, or personal services.

Because the rules surrounding government assistance programs can be complex, setting up a special needs trust often requires careful planning. Although some individuals attempt to create these trusts on their own, professional legal guidance is often recommended to ensure compliance with benefit regulations.

Comparison of Common Trust Types

| Trust Type | Purpose | Difficulty |

| Revocable Living Trust | Allows the grantor to control assets and avoid probate | Easy to Moderate |

| Irrevocable Trust | Protects assets and may reduce estate taxes | High |

| Testamentary Trust | Distributes assets according to instructions in a will | Moderate |

| Special Needs Trust | Supports a disabled beneficiary without affecting benefits | Moderate to High |

Understanding these trust options can help you determine which type best fits your estate planning goals. In many cases, individuals asking “can you set up a trust without an attorney” find that simpler trusts, such as revocable living trusts, are easier to create on their own, while more complex trusts may require professional legal assistance.

Step-by-Step Guide to Setting Up a Trust Without an Attorney

If you are wondering can you set up a trust without an attorney, the answer is yes—many people create a basic trust on their own, especially when their estate is simple. However, the process must be done carefully to make sure the trust is legally valid and properly funded.

Below is a clear step-by-step guide explaining how to set up a trust without a lawyer.

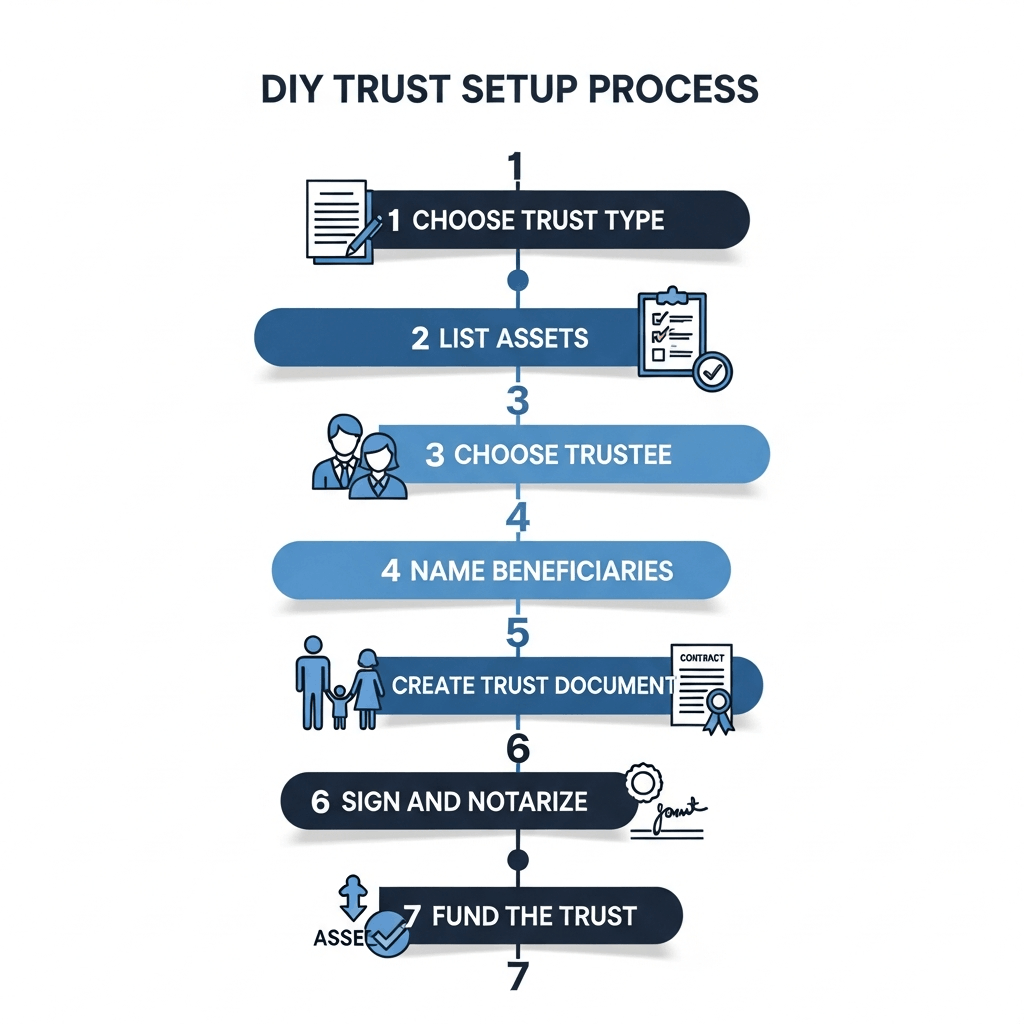

Step 1 — Decide the Type of Trust

The first step is choosing the type of trust that fits your estate planning goals. Different trusts serve different purposes, so selecting the right one is important before drafting any documents.

Common trust types include:

- Revocable living trust – The most common option that allows you to change or cancel the trust during your lifetime.

- Irrevocable trust – Once created, this trust usually cannot be changed and may offer tax or asset protection benefits.

- Testamentary trust – A trust created through a will that becomes active after your death.

- Special needs trust – Designed to provide financial support for a person with disabilities without affecting government benefits.

For most individuals creating a trust without an attorney, a revocable living trust is usually the simplest and most flexible choice.

Step 2 — List All Assets

Before creating the trust document, you should prepare a detailed list of all the assets you want to include in the trust. This helps you determine how the trust will be structured and ensures nothing important is overlooked.

Examples of assets that can be placed in a trust include:

- Real estate property

- Bank accounts

- Investment accounts

- Business interests

- Valuable personal property

Having a clear inventory of your assets will make it easier to transfer ownership to the trust later in the process.

Step 3 — Choose a Trustee

A trustee is the person or institution responsible for managing the trust and carrying out its instructions. When creating a trust yourself, choosing the right trustee is one of the most important decisions.

You can choose:

- Yourself as the initial trustee

- A trusted family member or friend

- A professional trustee such as a bank or financial institution

Many people who create a revocable living trust name themselves as the trustee during their lifetime and appoint a successor trustee who will take over after their death or if they become unable to manage the trust.

Step 4 — Name Beneficiaries

Beneficiaries are the individuals or organizations who will receive the assets held in the trust. Clearly identifying beneficiaries is essential to avoid confusion or disputes later.

When naming beneficiaries, you should specify:

- Full legal names

- Relationship to you

- Percentage or portion of assets they will receive

For example, a trust may distribute assets equally among children, or allocate specific property to certain individuals.

Step 5 — Create the Trust Document

The trust document is the legal agreement that establishes the trust and outlines how it will operate. If you are setting up a trust without an attorney, this document can be created using:

- Online legal platforms

- Trust-creation software

- DIY legal templates

The trust document typically includes:

- Name of the trust

- Grantor (the person creating the trust)

- Trustee and successor trustee

- Beneficiaries

- Instructions for managing and distributing assets

It is important that the document is clear, accurate, and consistent with your estate planning goals.

Step 6 — Sign and Notarize the Trust

Once the trust document is completed, it must be properly signed to become legally valid. Requirements may vary depending on your state, but generally the document should be:

- Signed by the grantor

- Witnessed by one or more individuals

- Notarized by a licensed notary public

Notarization helps confirm the authenticity of the document and may be required when transferring assets such as real estate into the trust.

Step 7 — Fund the Trust by Transferring Assets

Creating the trust document is only part of the process. The final and most important step is funding the trust, which means transferring ownership of assets into the trust.

This may include:

- Changing the title of real estate to the trust

- Moving bank accounts into the trust name

- Assigning investments or securities to the trust

- Transferring valuable personal property

If assets are not transferred properly, the trust may not function as intended. Many estate planning issues occur when people create a trust but forget to fund it.

By following these steps, it is possible to create a basic trust without legal assistance. However, if your estate includes complex assets, tax concerns, or large property holdings, consulting a qualified estate planning professional may still be beneficial.

Documents Required to Create a Trust

If you plan to create a trust on your own, gathering the right paperwork is an important first step. While many people ask whether you can set up a trust without an attorney, the process becomes much easier when you prepare all the necessary documents in advance. These documents help establish the trust legally and ensure that your assets are properly transferred into it.

Below are the key documents typically required when creating a trust.

Trust Agreement

The trust agreement is the most important document in the entire process. This legal document outlines how the trust will operate and who will be involved. It usually includes details such as the name of the trust, the grantor (the person creating the trust), the trustee who manages the trust, and the beneficiaries who will receive the assets.

The trust agreement also explains how assets will be distributed, when beneficiaries can access them, and what powers the trustee has. When creating a trust without an attorney, many people use templates or online legal tools to draft this document. However, it must be written clearly and follow the legal requirements of your state.

Property Titles

If you plan to place real estate into the trust, you will need the property titles or deeds. These documents prove ownership of the property and allow you to transfer that ownership to the trust.

For example, if you own a house, the title must be updated so that the trust becomes the legal owner instead of you personally. Without transferring the property title, the asset technically remains outside the trust, which could defeat the purpose of creating it.

Asset List

An asset list is another essential document when setting up a trust. This document provides a detailed inventory of everything you plan to include in the trust.

Common assets listed in a trust include:

- Real estate properties

- Bank accounts

- Investment accounts

- Business interests

- Valuable personal property

Creating a clear asset list helps ensure that nothing important is overlooked when transferring assets into the trust. It also makes the trustee’s job easier when managing or distributing those assets later.

Identification Documents

You will also need identification documents to verify the identity of the people involved in the trust. These documents may include government-issued IDs, such as a driver’s license or passport, along with other personal information required for legal records.

Identification is especially important when signing the trust agreement, opening trust bank accounts, or notarizing the document. Proper identification ensures that the trust is legally valid and recognized by financial institutions and government agencies.

Preparing these documents ahead of time can make the process much smoother if you decide to create a trust yourself. While it is possible to set up a trust without legal assistance, having complete and accurate documentation is critical to ensure that the trust works as intended.

How to Fund a Trust Properly

Creating a trust document is only the first step. To make the trust legally effective, you must fund the trust, which means transferring ownership of your assets into the trust. Many people create a trust but forget this step, which can make the trust useless. Even if you successfully answer the question “can you set up a trust without an attorney,” the trust will not work properly unless it is funded with your assets.

Funding a trust simply means changing the ownership of your assets so that the trust becomes the legal owner instead of you personally. Once assets are placed in the trust, the trustee manages them according to the instructions written in the trust document, and beneficiaries receive them according to the terms you set.

The process of funding a trust depends on the type of asset you want to transfer. Some assets require title changes, while others need updated ownership records or beneficiary designations. Below is a simple overview of how different assets are commonly transferred into a trust.

| Asset Type | How to Transfer to Trust |

| Real estate | Change the property title to the name of the trust through a new deed |

| Bank accounts | Update account ownership with the bank and list the trust as the owner |

| Investments | Transfer ownership of stocks, bonds, or brokerage accounts to the trust |

Transferring Real Estate to a Trust

To place real estate in a trust, you usually need to create and record a new property deed that transfers ownership from your name to the trust’s name. This process is commonly done through a quitclaim deed or warranty deed, depending on local laws. Once recorded with the appropriate government office, the property officially becomes part of the trust.

Moving Bank Accounts into a Trust

Bank accounts can typically be transferred by visiting your bank and requesting that the account ownership be updated to the trust. The bank may ask for a copy of the trust agreement or certification of trust before making the change.

Transferring Investments

Stocks, mutual funds, and brokerage accounts can be transferred by contacting the financial institution where the assets are held. In most cases, you will need to fill out ownership transfer forms so the account is registered in the name of the trust.

Why Funding a Trust Is Important

If assets are not transferred into the trust, they may still go through probate, which defeats one of the main purposes of creating a trust. Proper funding ensures that the trustee can manage the assets and distribute them according to your wishes without unnecessary legal complications.

By carefully transferring each asset into the trust, you ensure that your estate plan works as intended and that the trust provides the protection and control it was designed to offer.

Real Examples of Setting Up a Trust Without a Lawyer

Understanding how a trust works in real situations can make the process much easier. While many people hire attorneys for estate planning, some individuals successfully create simple trusts on their own when their financial situation is straightforward. Below are a few practical examples that illustrate how people may set up a trust without professional legal assistance.

Example 1 — Individual Creating a Living Trust

Consider an individual named John who owns a home, a savings account, and a small investment portfolio. John wants to ensure that his assets are passed directly to his sister after his death without going through probate. After researching estate planning options, he decides to create a revocable living trust on his own.

John drafts a trust document using an online estate planning tool. In the document, he names himself as the grantor and trustee, which means he keeps full control of his assets during his lifetime. He also names his sister as the beneficiary who will receive the assets after his passing.

Once the document is completed, John signs it and has it notarized according to his state’s requirements. He then transfers ownership of his home and investment account into the name of the trust. By doing this, John successfully sets up a simple living trust without hiring an attorney, allowing his assets to be distributed smoothly when the time comes.

Example 2 — Married Couple Estate Planning

A married couple, Sarah and David, want to ensure that their assets are protected and transferred efficiently to their children in the future. Their estate consists of a house, joint bank accounts, and retirement savings. Because their estate structure is relatively simple, they choose to create a joint revocable living trust themselves.

They begin by drafting a trust agreement that names both of them as co-grantors and co-trustees. This arrangement allows them to manage and control their assets together while they are alive. The trust document specifies that after the death of one spouse, the surviving spouse will continue managing the trust.

When both spouses pass away, the trust instructs that the remaining assets be distributed equally among their children. After signing and notarizing the trust agreement, Sarah and David transfer the ownership of their home and certain financial accounts into the trust. This step ensures the trust is properly funded and ready to function as intended.

Example 3 — Trust for Minor Children

Some parents create trusts to protect assets for their minor children. For example, Lisa, a single parent, wants to make sure her young daughter is financially secure if something happens to her. Instead of leaving assets directly to a minor, which can create legal complications, Lisa establishes a trust that will hold and manage the assets for her child.

Lisa creates a trust document naming herself as the grantor and her brother as the successor trustee. The trust states that if Lisa passes away, her brother will manage the funds for the child until she reaches a certain age, such as 21 or 25.

Lisa transfers a life insurance policy and a savings account into the trust. The document also includes instructions about how the funds can be used, such as for education, healthcare, and living expenses. This approach ensures the money is used responsibly for the child’s benefit until she becomes financially mature.

These examples show that it is possible to create a simple trust without legal assistance when the estate structure is straightforward. However, individuals with complex assets, business ownership, or significant tax considerations may still benefit from consulting an estate planning attorney to avoid costly mistakes.

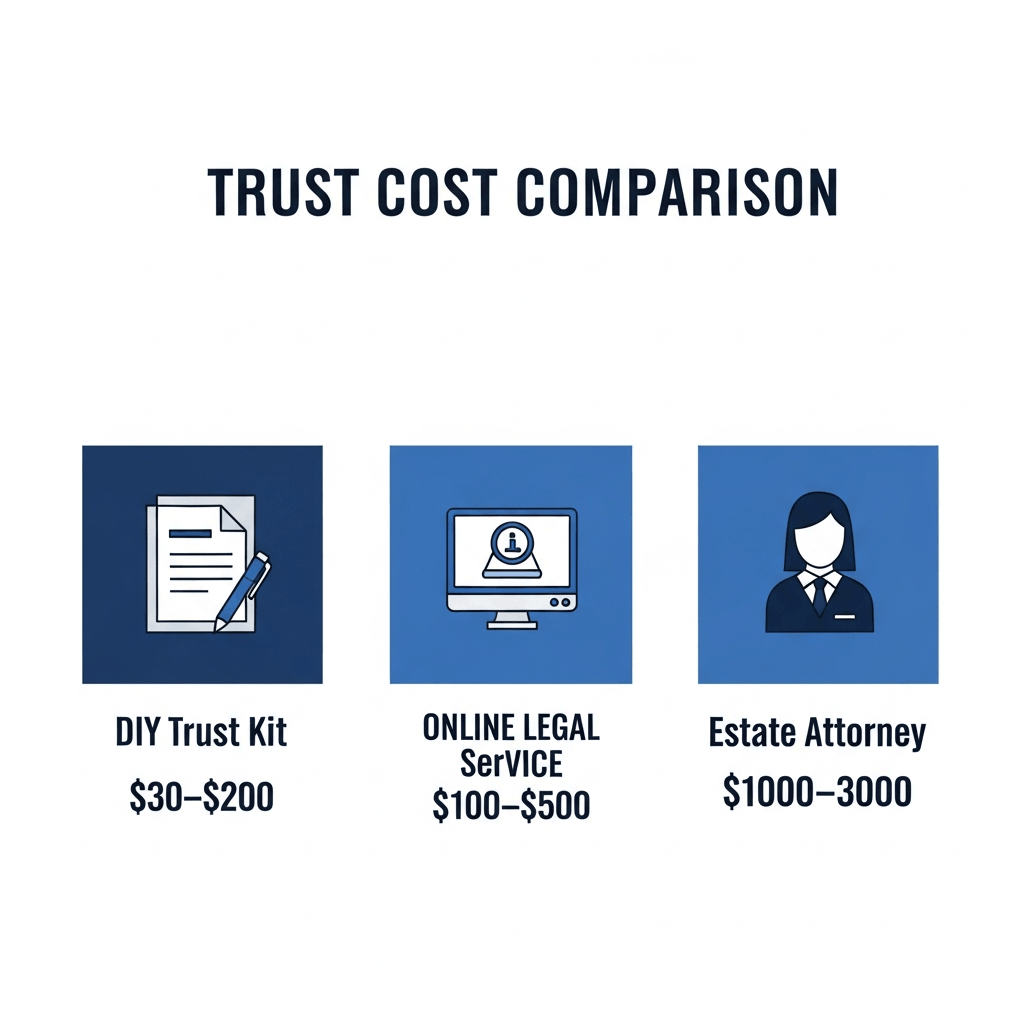

Cost of Setting Up a Trust Without an Attorney

One of the biggest reasons people consider creating a trust on their own is the potential cost savings. Hiring an estate planning attorney can be expensive, so many individuals explore DIY options or online services to set up a trust at a lower price. The total cost depends on the method you choose, the complexity of your estate, and the type of trust you want to create.

If you are wondering can you set up a trust without an attorney and how much it costs, the answer is yes—many people create a basic living trust using affordable tools or online platforms. However, while DIY methods are cheaper, they may not provide the same level of legal customization and protection as a trust drafted by an experienced lawyer.

Below is a general comparison of the most common ways to create a trust and their average costs.

| Method | Average Cost |

| DIY trust kit | $30–$200 |

| Online legal service | $100–$500 |

| Estate attorney | $1000–$3000 |

DIY Trust Kits

DIY trust kits are the most affordable option for people who want to create a simple trust without legal assistance. These kits usually include templates, instructions, and sample documents that guide you through the process of drafting a trust agreement. They are best suited for individuals with straightforward assets and uncomplicated estate plans.

However, DIY kits often provide limited customization, and mistakes in legal wording or asset transfers could create problems later.

Online Legal Services

Online legal platforms offer a middle-ground solution between DIY tools and hiring a lawyer. These services typically provide step-by-step questionnaires that generate customized trust documents based on your answers. Many platforms also include customer support or optional legal reviews.

This option works well for people who want more guidance than a DIY kit but still want to avoid the higher costs of hiring an attorney.

Hiring an Estate Planning Attorney

Working with an estate planning attorney is the most expensive option, but it also provides the highest level of legal accuracy and customization. Attorneys can help design complex trust structures, address tax issues, and ensure the trust complies with state laws.

For individuals with large estates, multiple properties, business interests, or complicated family situations, professional legal guidance is often worth the investment.

In short, while you can set up a trust without an attorney at a relatively low cost, it is important to consider the complexity of your estate and the potential risks before choosing a DIY approach.

Best Online Tools to Create a Trust Yourself

If you’re wondering can you set up a trust without an attorney, one of the easiest ways is by using reputable online estate-planning tools. These platforms provide guided questionnaires and legally formatted documents that help individuals create a trust without needing deep legal knowledge.

While online services cannot replace personalized legal advice, they can be a practical solution for people with simple estates and straightforward asset distribution plans. Below are some of the most popular platforms that help users create a trust on their own.

LegalZoom

LegalZoom is one of the most widely known online legal service providers. It offers step-by-step guidance to help users create a revocable living trust and other estate planning documents.

The platform asks a series of questions about your assets, beneficiaries, and trustees, then generates the appropriate legal documents based on your answers. LegalZoom also provides optional attorney support for reviewing documents if you want additional legal assurance.

Key features:

- Guided trust creation process

- Customizable estate planning documents

- Optional attorney review services

- Additional tools such as wills and power of attorney

This platform is often chosen by people who want a structured and user-friendly way to create a trust online.

Rocket Lawyer

Another popular option is Rocket Lawyer. It provides customizable legal documents and allows users to create a trust through an interactive document builder.

Rocket Lawyer stands out because it offers subscription-based access to legal documents and the option to ask legal questions to licensed attorneys.

Key features:

- Customizable trust document templates

- Access to legal advice from attorneys

- Document editing and storage tools

- Additional estate planning forms

For individuals exploring whether they can create a trust without a lawyer, Rocket Lawyer offers a flexible solution with optional professional support.

Trust & Will

Trust & Will focuses specifically on estate planning services. Unlike general legal platforms, it is designed primarily for creating wills and trusts online.

The platform simplifies the process by guiding users through a series of easy questions and generating legally compliant documents that can be printed and signed.

Key features:

- Specialized estate planning tools

- Easy step-by-step trust creation process

- Document storage and updates

- User-friendly interface for beginners

Trust & Will is often recommended for people who want a simple and straightforward approach to creating a trust without hiring an attorney.

Nolo Quicken WillMaker

Quicken WillMaker & Trust is one of the oldest and most trusted DIY estate planning tools. Developed by Nolo, this software allows users to create a wide range of legal documents, including living trusts.

Unlike web-based services, Quicken WillMaker is typically installed on a computer and provides detailed guidance throughout the estate planning process.

Key features:

- Comprehensive estate planning software

- Step-by-step interview format

- Multiple legal document templates

- One-time purchase rather than subscription

This tool is particularly useful for individuals who prefer offline software and a more detailed document creation process.

Choosing the Right Tool

Each of these tools can help answer the question “can you set up a trust without an attorney?” by providing structured guidance and legally formatted documents. However, the best option depends on your situation.

- If you want a well-known platform with optional attorney support, LegalZoom may be a good choice.

- If you prefer flexibility and ongoing legal access, Rocket Lawyer might be suitable.

- If you want a simple estate-planning-focused platform, Trust & Will is a popular option.

- If you prefer desktop software with comprehensive document templates, Quicken WillMaker is worth considering.

For people with complex estates, large assets, or tax concerns, consulting an estate planning attorney is still recommended. However, for straightforward situations, these online tools can make it much easier to create a trust yourself without hiring a lawyer.

Common Mistakes When Creating a Trust Without a Lawyer

Setting up a trust on your own can save money and give you more control over your estate planning. However, when people try to create a trust without professional legal guidance, they sometimes make mistakes that can affect the trust’s validity or effectiveness. If you plan to create a trust yourself, it is important to understand the most common pitfalls so you can avoid them.

Not Funding the Trust

One of the most common mistakes people make after creating a trust is failing to fund it. Creating a trust document alone is not enough. You must transfer your assets into the trust so that it legally owns them.

For example, if you create a living trust but leave your house, bank accounts, or investments in your personal name, those assets may still go through probate after your death. Funding a trust usually involves updating property titles, changing account ownership, or assigning assets to the trust. Without this step, the trust may not serve its intended purpose.

Using Incorrect Legal Language

Another common issue occurs when people use incorrect or unclear legal language in the trust document. Trust documents must clearly define the roles of the trustee, beneficiaries, and the instructions for managing and distributing assets.

If the wording is vague or legally incorrect, it can create confusion, disputes among beneficiaries, or even make the trust unenforceable. Many DIY templates exist online, but they may not always match your specific needs or comply with local legal requirements.

Choosing the Wrong Trustee

The trustee plays a critical role in managing and distributing the assets held in the trust. Choosing the wrong person for this role can lead to serious problems later.

A trustee should be someone who is responsible, trustworthy, and capable of handling financial and legal responsibilities. If a trustee lacks financial knowledge or fails to act in the best interests of the beneficiaries, it may lead to conflicts or mismanagement of the trust’s assets.

Ignoring State Laws

Trust laws can vary depending on the state where you live. Some states require specific signing procedures, notarization, or witnesses for trust documents to be legally valid.

When people create a trust without understanding their state’s legal requirements, they risk creating a document that may not hold up in court. It is important to review your state’s estate planning laws or use a legally compliant template to ensure the trust is properly created.

By understanding these common mistakes, individuals who choose the DIY route can reduce the risk of problems and create a more effective trust structure. Taking time to carefully plan, draft, and fund the trust can help ensure that it works as intended and protects your assets for your beneficiaries.

DIY Trust vs Attorney-Created Trust

When planning your estate, many people wonder whether they should create a trust themselves or hire a lawyer. Both options can help you establish a legally valid trust, but they differ significantly in terms of cost, accuracy, and flexibility. Understanding these differences can help you decide which option is best for your situation.

A DIY trust is created using online tools, templates, or trust kits without professional legal assistance. This option is usually more affordable and works well for people with simple estates. However, it requires careful attention to legal details to avoid mistakes.

On the other hand, an attorney-created trust is prepared by an experienced estate planning lawyer. While this option is more expensive, it offers greater legal accuracy and customization, especially for complex estates involving multiple assets, business ownership, or tax considerations.

Below is a comparison of the two options to help you understand their key differences.

| Factor | DIY Trust | Attorney-Created Trust |

| Cost | Low cost; usually between $30 and $500 depending on the tools used | High cost; typically $1,000 to $3,000 or more depending on complexity |

| Legal Accuracy | Moderate; depends on how well you follow instructions and understand legal requirements | High; prepared by a legal professional with knowledge of estate laws |

| Customization | Limited; templates may not address complex financial situations | Full customization based on your assets, family structure, and goals |

In simple situations, such as when you only need a basic revocable living trust, creating a trust yourself can be a practical and cost-effective option. However, if your estate includes significant assets, multiple beneficiaries, or complicated tax issues, working with an attorney can help ensure your trust is legally sound and tailored to your needs.

Choosing between a DIY trust and an attorney-created trust ultimately depends on the complexity of your estate, your budget, and how comfortable you are handling legal documents on your own.

State Laws You Should Know Before Creating a Trust

When planning a trust, it’s important to understand that trust laws vary by state. While the basic concept of a trust is recognized across the United States, each state has its own legal requirements for creating, signing, and managing a trust. These differences can affect how a trust is formed, whether notarization is required, and how assets are transferred into the trust.

This is one of the reasons people often ask: can you set up a trust without an attorney? The answer is yes, but you must make sure that the trust document complies with the specific laws of your state. Failing to follow state requirements could make the trust difficult to enforce or lead to legal disputes later.

Below are some examples of how trust laws can differ in major states.

California

In California, trusts are commonly used for estate planning because they help families avoid probate, which can be time-consuming and expensive. A trust document must clearly identify the grantor, trustee, and beneficiaries, and it must show the grantor’s intent to create the trust. While notarization is not always legally required for the trust document itself, it is often needed when transferring real estate into the trust.

California also requires that assets be properly funded into the trust, meaning property titles, bank accounts, or investments must be legally transferred to the trust’s name.

Texas

Texas law allows individuals to create both revocable and irrevocable trusts. A trust can be established through a written document that clearly outlines the trust terms and responsibilities of the trustee. In many cases, notarization is recommended to help verify the authenticity of the document.

Texas also recognizes living trusts as a useful tool to manage property and distribute assets after death without probate. However, similar to other states, the trust must be properly funded by transferring ownership of assets into the trust.

Florida

Florida has detailed statutes governing trusts, and it is known for having clear rules about trust administration and trustee responsibilities. A written trust agreement is typically required, and the grantor must have the legal capacity to create the trust.

Florida residents often use revocable living trusts to manage property and simplify estate transfers. While it is possible to create a trust without an attorney, individuals must ensure that the document meets Florida’s legal standards and that assets are properly placed into the trust.

New York

New York has more formal requirements compared to some other states. For example, a trust document often needs to be signed and acknowledged before a notary public, especially when it involves property transfers.

In addition, New York law requires that the trust terms clearly define the trustee’s powers and the rights of beneficiaries. Because of these stricter requirements, people creating a DIY trust in New York must pay close attention to the legal wording and documentation.

Understanding your state’s trust laws is essential before creating a DIY trust. Although it is possible to set up a trust without legal assistance, taking the time to research state-specific rules can help ensure that the trust is valid, enforceable, and properly structured.

Frequently Asked Questions

Is a DIY trust legally valid?

Yes, a DIY trust can be legally valid if it meets the legal requirements of your state. This usually includes creating a written trust document, naming a trustee and beneficiaries, signing the document properly, and transferring assets into the trust. However, mistakes in wording or asset transfers can cause legal problems later, which is why some people still choose to consult an attorney.

Can I create a trust online?

Yes, many people create trusts online using legal document platforms. These services provide templates and step-by-step guidance to help you draft a trust document, name beneficiaries, and complete the process. While online tools can simplify the process, they may not cover complex estate planning situations.

Do trusts need to be notarized?

In many cases, trust documents should be notarized to help prove their authenticity and prevent disputes in the future. Some states may also require witnesses when signing the trust document. Even if notarization is not legally required, it is often recommended because it strengthens the legal validity of the trust.

Can a trust replace a will?

A trust can manage and distribute assets without going through probate, but it does not always completely replace a will. Many people create a pour-over will alongside a trust to ensure that any assets not included in the trust are transferred into it after death. Using both documents together provides stronger estate planning protection.

What happens if a trust is not funded?

If a trust is not funded, it may not serve its intended purpose. Funding a trust means transferring ownership of assets—such as property, bank accounts, or investments—into the trust’s name. If this step is skipped, those assets may still go through probate and the trust may have little or no legal effect.

How long does it take to create a trust?

Creating a simple trust can take anywhere from a few hours to a few days if you use an online service or DIY trust template. However, the complete process may take longer because you also need to transfer assets into the trust. For more complex estates, the process can take several weeks.

What types of assets can be placed in a trust?

Many types of assets can be transferred into a trust, including real estate, bank accounts, investment accounts, business interests, and valuable personal property. Properly transferring these assets into the trust is an essential step to ensure the trust functions as intended.

Can I change or revoke a trust after creating it?

If you create a revocable living trust, you can usually change, update, or cancel it at any time while you are alive and mentally competent. However, an irrevocable trust is much harder to modify or revoke once it has been created, which is why careful planning is important before establishing one.

Final Thoughts

So, can you set up a trust without an attorney? The answer is yes. Many people create a basic trust on their own using online tools, legal templates, or DIY estate planning software. If your financial situation is simple and your assets are easy to transfer, setting up a trust without professional legal help can be a practical and cost-effective option.

However, the success of a DIY trust largely depends on the complexity of your estate. When you have multiple properties, significant investments, business ownership, or complicated family situations, the legal requirements can become more detailed. In these cases, even small mistakes in the trust document or asset transfer process could lead to legal disputes, tax issues, or problems for your beneficiaries in the future.

Before deciding to create a trust on your own, it is important to carefully evaluate your assets, understand the legal requirements in your state, and make sure the trust is properly funded. A well-structured trust can help protect your assets and simplify estate planning, but it must be created and managed correctly.

In short, setting up a trust without an attorney is possible, but it works best for straightforward estates. For more complex financial situations, consulting an experienced estate planning attorney may provide greater legal protection and peace of mind for you and your beneficiaries.